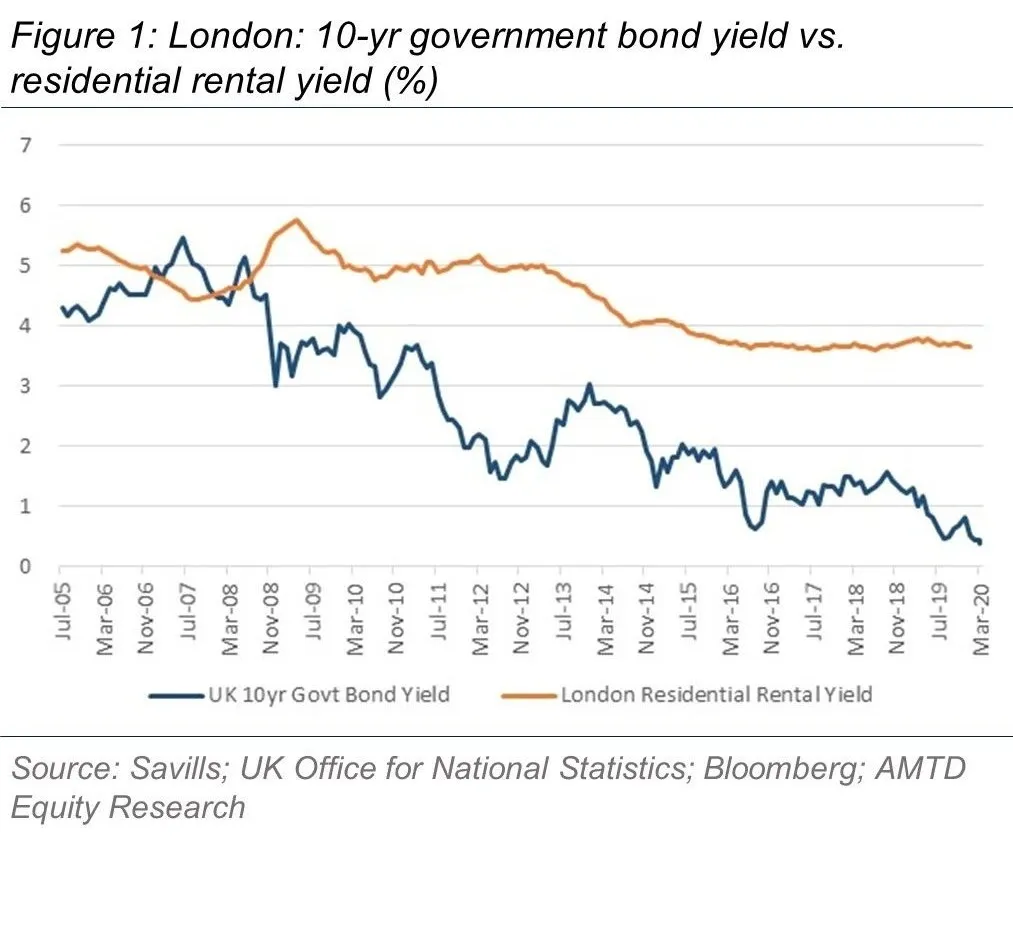

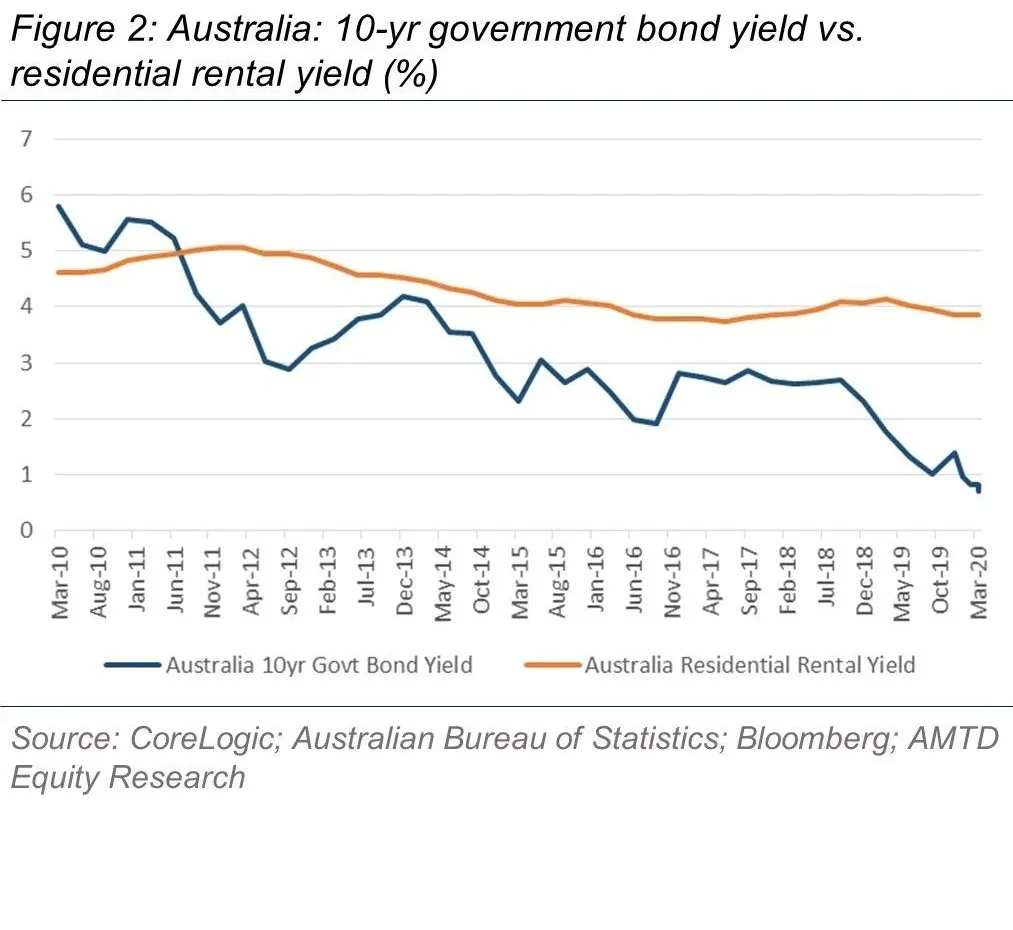

AMTD Research has published the report of FEC (35.HK). We reiterate Buy rating with a target price of HK$4.21/sh. With US Fed and Reserve Bank of Australia cutting rates in the last few days, we believe global property investors will scour the globe to chase for yield in the medium term. This should stimulate the UK and Australia property sales of Far East Consortium (FEC), following its recent launches of Consort Place in London and Queen’s Wharf Brisbane.

Asset inflation trend will attract global property investors

Property is often considered as a relatively safe asset class and is almost a must have for Global High Net Worth Individuals in their portfolio. As central banks around the world cut their countries’ respective benchmark rates (US Fed by 50bps and RBA by 25bps) we expect the lower borrowing costs will drive rental yields lower, resulting in property asset inflation in the medium term. We believe that FEC is well poised to capture this trend with their recently launched property projects in London Canary Wharf and Brisbane in Australia, respectively. We estimate that UK and Australia contribute to ~80% of FEC FY20E property development revenues. Depending on the project, global property investors can contribute up to ~50% of such property sales.

Consort Place London: A gem at the heart of Canary Wharf

FEC recently launched Consort Place for sale in Feb 2020, a project that is at the heart of Canary Wharf, neighbouring the London headquarters of JP Morgan, HSBC, Morgan Stanley, etc. Consort Place is a 390,000 sqft mixed-used residential development project and we believe it is on track to be a key FY2020-2021 sales contributor with a GDV of ~HK$4bn, with an ASP of ~GBP1,000-1,100/sqft.

Queen’s Wharf Bisbane: A scarce Resi/Com/Hotel/Casino Development

The developer has also launched its Queen’s Wharf Brisbane project for sale in Feb 2020, which was well received by the market despite the COVID-19 outbreak. The project is also mixed-used development comprising of residential, hotel and a casino, overlooking the Brisbane river. Phase 1 was recently launched with 252,000 sqft and is expecting to achieve a total GDV of ~HK$3.3bn.

Hotel portfolio face challenges, but manageable as cap rate compresses

COVID-19 outbreak is putting pressure on the company’s hotel portfolio, with occupancy rates under pressure. However, we believe the cashflow and earnings impact is manageable, as property development is the main earnings driver contributing to 56% of FY20E Total Revenues, vs ~27% from Hotels. From an asset value perspective, while Hotels contribute to ~52% of our SOTP GAV, the rate cuts will also help to mitigate the rental pressures as cap rate is expected to compress.

Stock offering 6.3% div yield, at 5.5x FY20E P/E, 0.6x FY20E P/B

We believe Far East Consortium is trading at attractive valuations of 5.5x FY20E P/E and a 0.6x FY20E P/B. The values are mostly at cost, as hotels are not marked to market under the accounting rules. This makes the valuation all the more attractive, considering that it is trading at a same P/B with other HK property developers who have a large investment property portfolio which is marked-to-market on their books.

The Summary is solely for AMTD clients’ information. A person will not be regarded by AMTD as its client solely because he or she receives this Summary. The contents of the Summary will not constitute investment recommendations to any person in any event. AMTD will not assume any legal responsibilities regarding any consequences or losses arising from the direct or indirect use of the Summary, or investment made accordingly.

The extracted valuations, forecasts and ratings in the Summary represents the judgments or opinions formed on the issuance date of the Report. The contents of the Summary may become inaccurate or invalid as a result of changes in circumstances or other factors subsequent to the issuance of the Report. AMTD is not obliged to update inaccurate or outdated information subsequently. Meanwhile, AMTD will not separately inform the readers of the Summary after updates have been made.

AMTD reserves the copyrights of the contents of the Summary. No part of the Report shall be forwarded, modified, quoted, copied or reproduced in any form by any mean to any other person without the prior written consent of AMTD. The Company retains all legal rights in this Report.

We, Jacky Chan and Karen Huang, hereby certify that (i) all of the views expressed in this research report reflect accurately our personal views about the subject company or companies and its or their securities; and (ii) no part of our compensation was, is or will be, directly or indirectly, related to the specific recommendations or views expressed by us in this research report, nor is it tied to any specific investment banking transactions performed by AMTD Global Markets Limited.

Firm Disclosure

AMTD Global Markets Limited has an investment banking relationship with Far East Consortium International Limited and/or their affiliate(s) within the past 12 months.

AMTD Global Markets Limited

Address: 23/F – 25/F, Nexxus Building, No. 41 Connaught Road Central, Central, Hong Kong

Tel: (852) 3163-3288 Fax: (852) 3163-3289

This research report provides general information only and is not to be construed as an offer to sell or a solicitation of an offer to buy any security in any jurisdiction where such offer or solicitation would be illegal. It does not (i) constitute a personal advice or recommendation, including but not limited to accounting, legal or tax advice, or investment recommendations; or (ii) take into account any specific clients’ particular needs, investment objectives and financial situation. AMTD does not act as an adviser and it accepts no fiduciary responsibility or liability for any financial or other consequences. This research report should not be taken in substitution for judgment to be exercised by clients. Clients should consider if any information, advice or recommendation in this research report is suitable for their particular circumstances and seek legal or professional advice, if appropriate.

This research report is based on information from sources that we considered reliable. We do not warrant its completeness or accuracy except with respect to any disclosures relative to AMTD and/or its affiliates. The value or price of investments referred to in this research report and the return from them may fluctuate. Past performance is not reliable indicator to future performance. Future returns are not guaranteed and a loss of original capital may occur.

The facts, estimates, opinions, forecasts and any other information contained in the research report are as of the date hereof and are subject to change without prior notification. AMTD, its group companies, or any of its or their directors or employees (“AMTD Group”) do not represent or warrant, expressly or impliedly, that the information contained in the research report is correct, accurate or complete and it should not be relied upon. AMTD Group will accept no responsibilities or liabilities whatsoever for any use of or reliance upon the research report and its contents.

This research report may contain information from third parties, such as credit ratings from credit ratings agencies. The reproduction and redistribution of the third party content in any form by any means is forbidden except with prior written consent from the relevant third party. Third party content providers do not guarantee the timeliness, completeness, accuracy or availability of any information. They are not responsible for any errors or omissions, regardless of the cause, or for the results obtained from the use of such content. Third party content providers give no express or implied warranties, including, but not limited to, any warranties of merchantability of fitness for a particular purpose or use. Third party content providers shall not be liable for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including lost income or profits and opportunity costs) in connection with any use of their content. Credit ratings are statements of opinions and are not statements of fact or recommendations to purchase, hold or sell securities. They do not address the suitability of securities for investment purposes, and should not be relied on as investment advice.

To the extent allowed by relevant and applicable law and/or regulation: (i) AMTD, and/or its directors and employees may deal as principal or agent, or buy or sell, or have long or short positions in, the securities or other instruments based thereon, of issuers or securities mentioned herein; (ii) AMTD may take part or make investment in financing transactions with, or provide other services to or solicit business from issuer(s) of the securities mentioned in the research report; (iii) AMTD may make a market in the securities in respect of the issuer mentioned in the research report; (iv) AMTD may have served as manager or co-manager of a public offering of securities for, or currently may make a primary market in issues of, any or all of the entities mentioned in this research report or may be providing, or have provided within the previous 12 months, other investment banking services, or investment services in relation to the investment concerned or a related investment.

AMTD controls information flow and manages conflicts of interest through its compliance policies and procedures (such as, Chinese Wall maintenance and staff dealing monitoring).

The research report is strictly confidential to the recipient. No part of this research report may be reproduced or redistributed in any form by any means to any other person without the prior written consent of AMTD Global Markets Limited.